ERA Group's freight newsletter covers a summary of current industry topics; market trends; freight service provider financial results; and a view to the future for major freight industry segments.

Current industry topics

Non-Domiciled Commercial Driver’s Licenses

So; what are they? A non-domiciled Commercial Driver’s License (CDL) is issued to individuals who are not permanent residents of the state where the license is obtained; typically foreign nationals legally present in the U.S.

In response to the Federal Motor Carrier Safety Administration (FMCSA) audit that uncovered widespread non-compliance to existing regulations in multiple states – additionally linking at least five fatal crashes this year to non-domiciled CDL holders - the Department of Transportation issued an emergency order that states must immediately stop issuing or renewing CDL’s until new federal regulations are in place. Hopefully; this action will result in greater highway safety.

From an industry standpoint; this change will take some capacity out of the market; as it is estimated that there are at least 200;000 Non-Domiciled CDL holders in the U.S. The impact on the freight industry has not yet been felt; but it will be.

Artificial Intelligence

Arguably; there is no hotter topic in the country today than Artificial Intelligence. AI’s impact is already being felt in many facets of everyday life. The Freight Industry is no different. While AI today is not driving 18-wheelers down our highways; it is being embedded in the overall logistics process. Perhaps the most prominent reference comes with C.H. Robinson’s recent quarterly results -

“We are innovating to harness the power of artificial intelligence and driving automation across the full lifecycle of a load; which gives our customers better service; while also helping us improve our performance by automating tasks that free up our talented people to work on more strategic and higher value work."

Tariffs On; Tariffs Off

While the subject of Tariffs may not top AI overall; it is certainly top of mind. The #1 tariff issue causing heartburn for shippers today is uncertainty. The term consistency will likely be used less and less frequently. From shipment peaks and valleys due to customer inventory swings; to new lanes covering new product and material sources; and everything in between – change is the operative word going forward.

Key takeaway: The topics above; and others not detailed; demand that shippers must focus on flexibility in their logistics function to meet the continuing series of challenges that will present themselves.

The Market - Truckload Rates; Diesel Fuel Prices

Two barometers of the Freight market over time are Truckload Linehaul Rates per Mile and Diesel Fuel Price per Gallon. The charts below were developed using data from the Department of Energy and from DAT Freight and Analytics.

Coming down from postpandemic peaks; Truckload Linehaul Rates per Mile have stabilized since Jan-24 • Van Linehaul Rates per Mile have ranged between $1.42 to $1.67 • Flatbed Rates per Mile have ranged between $1.90 to $2.12 Coming down from the steep rise in Diesel Fuel Prices due to Russia’s invasion of Ukraine; the Average Diesel Fuel Price per Gallon has stabilized since Jan-24; ranging between $3.49 and $4.04.

Key takeaway: While volatility in Linehaul Rates and Diesel Fuel Prices has lessened over recent history; the charts above show that extraordinary events can cause major shifts in the market. Shippers need to be ready to react quickly to marketplace changes.

What the numbers say

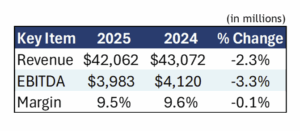

One way to assess the state of the freight industry is to review recent financial results from key players. The table below summarizes North American Financial Results for 15 large industry players; comparing the first half of 2025 to the first half of 2024.

The table illustrates that this is a difficult time period for Freight Service Providers. While Revenues and Profits (EBITDA) are down Margins were nearly flat as companies mostly offset the drop in revenues by containing costs.

A deeper dive is in order into four of the largest and most recognizable Freight Service Providers; summarized in the table below.

A few observations:

- At -4.7% year over year; Revenues for these top 4 providers were down nearly double the overall average of -2.3%. J.B Hunt was nearly flat due to the strength of their intermodal business.

- EBITDA was down 5.1%; mitigated by the +31.7% improvement at C.H. Robinson due to stringent cost-cutting measures

- At a 26.6% margin; Old Dominion was by far the most profitable provider; more than twice the overall average of 10.8%.

Key takeaway: The financial results above clearly demonstrate that the market continues to favour shippers over freight service providers.

The road ahead

For the remainder of 2025 through at least the 1st half of 2026; supply of freight services will exceed demand for freight services – the market will favour the shipper; not the freight service provider. Below; we captured key takeaways from multiple freight industry forecasts as we head into 2026; organized by service type.

Truckload

- Demand will remain weak at least through the 1st half of 2026 as the industry suffers from tariff-induced declines of retail imports and contraction of manufacturing.

- Supply continues to exceed demand with relief coming from new truck orders below replacement level orders; carriers exiting the market due to lower profits; and driver shortages stemming from enhanced regulations (Non-Domiciled CDL’s).

- As supply shrinks to rebalance with demand; rates will likely show modest upward movement in the latter half of 2026.

LTL

- Demand will remain weak through the end of 2025; with a limited rebound in early 2026 driven by restocking of lean retail inventories and the continued growth of E-commerce.

- Excess supply will continue to linger through all of 2026 as major carriers continue to report tonnage declines along with a continuing shortfall in drivers – the driver shortfall is projected to reach 160;000 by 2030.

- Rates will hold firm despite the drop in demand as freight service providers look to pass along labour and other cost increases to shippers.

Intermodal

- Demand is projected to remain weak through 2026 with small single digit percentage declines likely; as tariffs have negatively impacted import volumes reducing the need for Intermodal service.

- Equipment supply is adequate to meet the reduced demand with no major shortages anticipated in high-volume corridors.

- Excess supply will continue to hold rates down with no likely increases at least through mid-2026.

Key takeaway: What does this mean? Now is the time to lock down rates and service partners with favorable contracts before demand and supply return to equilibrium.